|

The current economic climate is facing higher inflation than previously expected, as indicated by increases in both the Producer Price Index (PPI) and Consumer Price Index (CPI). PPI indicates the cost of production from a producer standpoint while CPI reflects cost of living for consumers. On October 12th, CPI was reported to rise 0.4% on the month, above 0.3% forecast. The PPI increased 0.5% for September, against the estimated 0.3% rise. Several factors are contributing to this inflationary trend, including the persistent high cost of oil due to OPEC’s supply restriction and corporate consolidations in the oil sector, ongoing labor strikes, and a highly competitive job market. Federal Reserve Chairman Powell, in his address on October 19th, offered limited insight into the Fed’s outlook, but highlighted prevailing uncertainties. Due to elevated inflation, Powell hinted at the possibility of maintaining the current interest rate of 5.25% - 5.50% at the November 1st meeting further extending the period of high interest rates. The Federal Reserve, adopting a cautious stance, is prepared to reassess the situation during their meeting on December 13th if necessary.

Adding to the complexity is the ongoing conflict in the Middle East. A seminar hosted by Fidelity (script available in the source section) emphasized a probable escalation of tensions between Israel and Palestine due to the decisive determination of removing Hamas-controlled Gaza. The problem is rooted in the complex territorial landscape of Gaza. Twenty-five-mile land encompassing 2 million people, operates on two distinct levels. The first is the visible, densely populated urban area that exists on the surface. The second is the "subterranean" Gaza, an underground region primarily utilized for weapon manufacturing. Since the area is heavily urbanized, this possess a challenge to the Israeli army when it comes to deterring terroristic group while preserving lives of all civilians. An escalation is said to cause supply chain disturbance causing the oil prices to increase back to September levels. On October 19th, oil prices saw a moderate increase of 2.47%. With the situation evolving, a short-term gradual uptrend is anticipated within the industry. Despite losing their relevance, the monthlong auto strikes are continuing with union demand for substantial pay and benefits. Although production and revenues are impacted, a resolution is anticipated once demands are met, marking a pathway to recovery. Overall, the Federal Reserve is exercising caution. The risk of over-tightening is balanced with the need for inflation control. The Fed is likely awaiting October's CPI and PPI data to gain clearer insights into inflation trends. Despite energy market fluctuation, there is a promising sign in real estate. With the 10-year note yield above median cap rate, bonds offer more attractive returns. This gives an opportunity for investors to reallocate assets and “meet” the supply of bonds thus creating an equilibrium in which supply equals demand. This would bolster confidence in government fiscal policy and economic stability, potentially eliminating the need to raise interest rates. However, at Traditions Wealth Advisors we have diversified your portfolios well to buffer against inflation and protect against geo-political events like Israel and Ukraine. Source: https://www.crossmarkglobal.com/wp-content/uploads/A-Message-from-Bob-Ramifications-from-Middle-East-War.pdf https://institutional.fidelity.com/app/literature/item/9910988.html

0 Comments

Israel is in the midst of dealing with internal unrest while simultaneously engaging in key diplomatic discussions with Saudi Arabia and the U.S. These negotiations are especially significant as they could mark a turning point in the historic relations between Arab nations and Israel, with the potential recognition from Saudi Arabia recognizing Israel as a state. The U.S. is helping facilitate these discussions along with Saudi Arabia's proposal to boost oil production to “cement” this deal. However, a recent act of aggression from Hamas has introduced new challenges. Gaza, under the aegis of Hamas since 2007, has endured persistent economic adversities. Iran’s sponsorship of Hamas is viewed with suspicion, raising concerns about potential interferences in the ongoing Israel-centric diplomatic discussions. Although sanctions could be applied to Iran through similar pacts as JCPOA, Iran's strategic diversification of its economy since the 1980s has reduced the impact of such restrictive measures.

Simultaneously, adverse reactions from Israel could jeopardize the emerging diplomatic ties with Saudi Arabia and subsequently influence the proposed augmentation in oil output. The economic repercussions of the unfolding conflict are contingent upon its duration and scope. With the “battleground” located away from oil extraction sites, the initial 5% hike in oil prices on Monday, October 9th was a reflexive market reaction rather than a sustained trend (speculation). Subsequent days (October 10th and 11th) saw a retraction in oil prices nearing the last week’s levels. The economic outlook, particularly concerning oil prices, depends largely on the containment of the conflict within its current boundaries. An escalation spreading to other parts of the Middle East could influence a tangible shock in oil prices. However, historical context offers some reassurance; since 2007, the area has experienced four major wars and numerous minor conflicts, each lasting about a month on average, without causing prolonged disturbances in oil prices. On top of that, with winter season approaching, a seasonal dip in demand could serve as a stabilizing factor, potentially offsetting any short-term spikes in oil prices resulting from the conflict. How does this conflict compare to the 1970s? During the late 1960s and early 1970s, the Middle East was amidst geopolitical tensions. In 1973, the conflict escalated between the Arab (Egypt and Syria) and Israeli, known as the Yom Kippur War. With the U.S. intervention, $2.2 billion emergency financial aid package was sent to Israel, which prompted OPEC to impose an oil embargo against the U.S. This embargo brought more economic downturn in the U.S., exacerbating the already fragile economic environment partially triggered by Nixon’s detachment from the gold standard. Subsequently, the U.S. economy faced inflated oil prices, a supply shock, and severe energy shortages, exacerbating inflationary pressures and limiting economic growth—a phenomenon encapsulated in the term "stagflation." The latest geopolitical turmoil in Israel vastly differs from the past. The U.S. currently relies less on OPEC, the EIA (U.S. Energy Information Administration) data shows a decline to 15% bpd (barrels per day) of total oil imports from 47.8% bpd in 1973, with Canada now being the predominant supplier of 52.5% bpd. In short-term, the U.S. oil supply should remain stable unless the conflict expands. Long-term effects hinge on the Ukrainian crisis and potential Israeli-Saudi diplomatic relations. As time progresses, we will continue to monitor this situation and forewarn clients of emerging challenges. Source:https://www.eia.gov/energyexplained/oil-and-petroleum-products/imports-and-exports.php#:~:text=Since%201977%2C%20the%20percentage%20shares,of%20U.S.%20crude%20oil%20imports Traditions Wealth Advisors is starting a new series of weekly updates to our economy. We hired a new student intern to fulfill this need for our clients. Brien L. Smith, CEO of TWA, and Kristina Badrak, Economic Analyst Intern, will be informing you weekly of updates in the current market. Below is week 1, September 27, 2023:

In light of recent market fluctuations and continuous hikes in interest rates, there is a growing apprehension about a potential recession on the horizon. In this monthly edition of the TWA newsletter, we offer insights into the prevailing economic and financial market conditions and any implications it carries for investors.

Sources: https://www.chase.com/content/dam/chase-ux/documents/personal/investments/mid-year-outlook-2023.pdf  Brien is pictured above with the 2023-24 officers of the TAMU Economics Society. Over 50 members attended the meeting, and Brien presented on Financial Planning/Wealth Management as a Career. Thanks and Gig'em to the TAMU Economics Society for inviting TWA to their meeting.

Laurie received her BBA in Accounting from Texas A&M University in 1989. She worked in the audit department for Arthur Andersen in the San Antonio office from 1989-1991 and earned her CPA license in 1991. She has spent the majority of her professional career in Russellville, Arkansas, where her husband was employed at a 2-unit nuclear plant. After taking a few years off to start a family, Laurie worked in the business office of a rural community mental health center with services and facilities in 6 Arkansas counties from 1996-2005. In this position, she was responsible for the accounting functions of the agency, 2 HUD apartment complexes and 2 HUD

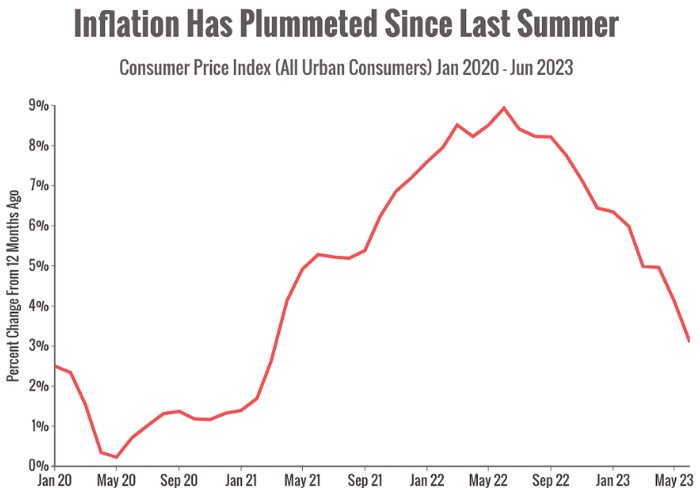

group home facilities, as well as applying for State grants. Laurie later worked for Kent Dollar and Associates, a local CPA firm from 2005-2007. After taking a few years off to focus on family needs, Laurie worked for Debbie Brown CPA PA in office from 2011 to 2017 and then worked remotely from 2018-2022 when her family moved to College Station. Her primary job duties were performing rural water company audits and the write up work, payroll functions, and tax returns for many small business S-Corporations. Laurie is married and has 3 young adult children. Laurie is a member of the Brazos County Aggie Moms Club and serves on the "Aggies in Need" committee. Laurie and her husband, Darrell, enjoy a variety of Aggie sporting events together and host family and close friends at their home and tailgate on Aggie football weekends. Laurie is also active at her church in many areas including the Women's ACTS retreat team, the bookstore, and welcoming people as a Front Door Disciple. She also enjoys helping at many Knights of Columbus events in the community. Laurie is excited to be a part of the team at Traditions Wealth Advisors and looks forward to assisting Brien with the many aspects of financial and tax planning for the clients. A word about recessions. Are we still going to see one this year? Let's discuss. Why did so many people think a recession was coming? Inflation and interest rates, primarily. Historically high inflation has cast a pall over the economy since early 2021. In response, the Federal Reserve has raised interest rates rapidly to bring inflation back down. Analysts worried those rapid interest rate hikes could trigger a "hard landing" recession.  But it looks like the dark mood is lifting. You can see in the chart above that inflation has been on a definite downward trend since last summer. That trend suggests that the Fed's interest rate program has worked to tame inflation.

So, will the Fed keep raising interest rates? Hard to say. The Fed raised interest rates again by a quarter of a point at its July meeting, but it's possible that it won't raise rates again if inflation remains on a downward trajectory. In fact, some analysts think that the Fed's next move might be to lower rates in 2024. Does that mean a recession is definitely off the table? That's far too optimistic. While the economy has been much, much more resilient than even seasoned analysts predicted, the accumulated effects of interest hikes may still deal a serious blow to growth. There are signs that the economy is weakening in some areas. For example, while American consumers are still spending, they aren't buying as much stuff. That's hurting the manufacturing sector, which has been in a slump for a while. Since consumer spending is worth about 70% of economic activity in the U.S. it’s an important indicator for future economic growth. Employment trends will also be important to watch. So far, the work of lowering inflation seems to have succeeded without damaging the job market. However, there are signs that the labor market may be weakening, so that's something to keep an eye on. Bottom line: things seem to be looking up. The dark clouds on the horizon appear to be breaking and there are reasons to be optimistic. But, it won't be smooth sailing. Is it ever? I'm keeping an eye on trends and I'll reach out as needed. Questions? Don't hesitate to reach out, Brien@traditionswealthadvisors.com Source: Life Strategy Financial. Munoz, Juan. 2 August 2023.  The number of fraud cases reported in 2022 was down year-over-year but the amount of money lost to scams was up—to $8.8 billion from $6.1 billion in 2021. The most prevalent scams were those dealing with investments. Imposter scams were the second most-common, followed by online shopping scams.

To help yourself stay safe, remember these guidelines:

One aspect of financial planning is considering the tax impacts of investment decisions. New rules for catch-up contributions, as shown in Anne Tergesen’s article, “High Earners to Lose A 401(k) Tax Break”, will change the tax impact for savers, especially those in higher tax brackets. Earners saving for retirement, ages 50 and over, are able to make additional contributions to their 401(k)s annually. Next year, these catch-up contributions must go into a Roth IRA account. The old rules allowed taxpayers to avoid paying taxes on these contributions at their current, higher tax rate and pay taxes on the earnings in retirement, when they will hopefully have lower tax rates. They could also take a deduction on these contributions. Now, the taxes must be paid upfront, and taxpayers lose this deduction. This means the contributions will be taxed at the earners current tax rate, not favorable for those in higher tax brackets, and they do not get tax saving in their current year.

However, there are benefits to this money being put into a Roth IRA. The biggest advantage is that any growth from the Roth IRA is tax-free. So, while this change may decrease tax savings in the current year, there would be no tax eating away at the realized Roth IRA investment in retirement. These changes are set for next year, but many have asked for delay to address some complications that these new rules pose. Some companies have to rework their systems to ensure the catch-up money in going into a Roth. Other companies did not previously have a Roth as an option for employees, which if unchanged, would cause those workers to forfeit any catch-up contributions. Companies are also unsure if under these new rules if they still need to ask permission to put this money into a Roth, or if it can be done automatically. Time will tell the true impacts of these new rules, but it will certainly have an impact on strategic planning for retirement. Questions on this article or to find out more, e-mail Brien@TraditionsWealthAdvisor.com or visit: https://www.wsj.com/articles/retirement-tax-breaks-401k-contributions-2868ffdc  You may still be breathing a sigh of relief about completing your taxes for 2022, and relishing the thought that you don't have to think about filing for many months to come. But with summer fast approaching, it's a great time to start lining up your strategy to help reduce your 2023 tax bill. Starting early can pay off when it's time to file next April.

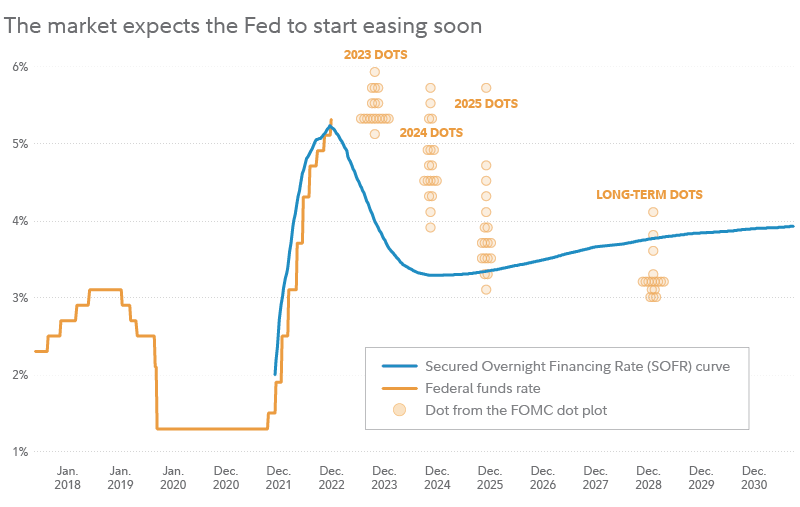

Here are 6 tax-planning strategies to consider: 1. Examine your W-4 withholdings 2. Look for tax losses to harvest 3. Reconsider itemizing 4. Boost your pre-tax contributions 5. Plan for RMDs 6. Consider a Roth conversion Everyone's tax situation is different, and it makes sense to consult with a tax expert or advisor to come up with a financial plan that works for you. With a little planning this summer, you can rest easy knowing that come tax time, you'll be prepared. For more information on each of these tax tips, click this link or contact us at Brien@TraditionsWealthAdvisors.com  The Fed raised rates as expected last week, and the broad consensus among investors and in the markets is that it was the last rate hike for this cycle. (The Fed itself didn’t commit to an end to rate hikes, but it did signal that pausing here is a very real possibility.) While last week’s hike was broadly expected by markets—just as an end to the hikes at this point is broadly expected—what comes next is more of an open question. According to expectations priced into markets (which, granted, in fact are often wrong), the Fed will start a campaign of cutting rates, as shown below in the blue line. Given how high inflation still is, and how resilient the economy still seems to be, I think that may be wishful thinking.  Why does the market expect the Fed to imminently drop rates back to 3% or below? Perhaps it’s flawed modeling by bond traders. Or perhaps they are just using the average of all cycles. Historically, the Fed more often than not starts easing soon after its final rate hike. In fact, the forward interest-rate curve above looks almost identical to the average easing cycle that typically follows the peak of a rate-hike cycle. How important is this disconnect? It may depend on where the economy, and inflation, go from here. If inflation continues to improve and the economy stays resilient, rates that are higher for longer could prove benign for markets. On the other hand, if inflation becomes stubborn and the economy weakens, then that disconnect could become significant. Have rates gone high enough?In very simple terms, the Fed’s new 5% to 5.25% target range for the fed funds rate is the highest it’s been since 2007. But with inflation still elevated, are rates restrictive enough? Based on my own calculations of what would be a “neutral” fed funds rate (meaning one that is neither restrictive nor accommodative), the Fed is moderately restrictive—with the current fed funds rate about 1 percentage point above neutral. Another way of looking at it is by comparing the policy rate to the inflation rate. The Fed’s current target rate is now also above the 4.6% annual rate of change in the core Personal Consumption Expenditures Price Index (which measures price inflation felt by consumers, excluding food and energy, which tend to be more volatile). So by that definition the Fed is also moderately restrictive. But based on the chart below, since the 1970s the Fed has generally raised rates to above the peak in headline inflation. So depending on which exact inflation measure one uses, by that standard the Fed may still be accommodative. Some signs of a soft landingFirst-quarter earnings season is now heading toward the finish line, and the results have been strong. Out of the 425 companies that had reported by last week, 78% have beaten estimates—beating them by an average of 6.72 percentage points. It’s hard to see this earnings season as a glass half-empty. The strength in earnings is supported by the fact that revenues continue to march to new highs (at least in nominal, or non-inflation-adjusted, terms). And with revenues trending higher and earnings growth starting to flatten out, by definition it also means that profit margins are stabilizing. Yet the market isn’t acting like a bull marketConsensus earnings estimates are suggesting that the US is headed for a soft landing. And this earnings season showed some encouraging signs. But not all signs are pointing in the same direction. While the S&P® 500 is up more than 8% so far this year (and around double that since the market’s October low), there is uneven participation beneath the surface. Early-cycle bull markets tend to be driven by segments and styles that are more economically sensitive and more volatile. Small- and microcap indexes are usually in or close to the lead in an early bull market—posting strong performance and usually beating larger-cap indexes like the S&P 500. But not this time. Relative performance of Russell Microcap index to S&P 500 is taken by dividing the level of the Russell Microcap index by the level of the S&P 500 index. Source: FMRCo., Bloomberg, Haver. The weakness in small caps and microcaps is not consistent with the idea that an early-cycle bull market is sprouting, and continues to cast at least some doubt on where we go from here. That—along with expectations for the Fed—is among the key inconsistencies facing this moment in the markets, and why this still doesn’t look like the start of a new bull market. Source: Fidelity Viewpoints. Timmer, Jurrien. 11 May 2023. https://www.fidelity.com/learning-center/trading-investing/interest-rates-peaked?ccsource=email_weekly_0511_1037578_43_0_CV1 |

Let our team work for you. Call 979-694-9100 or

email Michael@TraditionsWealthAdvisors.com

|

TRADITIONS WEALTH ADVISORS

2700 Earl Rudder Frwy South, Ste. 2600 College Station, TX 77845 |

VISIT OUR BLOG: Stay current with industry news and tips.

|