|

As we close out 2022 and ring in 2023, there are some choices you can make to possibly lower your taxes. Consider these tips before year-end to help your 2022 taxes and beyond.

1. Contribute to tax-advantaged accounts. You must make your final contributions to a 401(k) or 403(b) by December 31st. You can contribute up to $20,500 before taxes. If you're 50 or over, you can make additional catch-up contributions of $6,500. That money reduces your taxable income dollar for dollar. And don't forget about health savings accounts (HSAs) if you have a high-deductible health plan. While you have until the April tax filing deadline to contribute, you can put away up to $3,650 for an individual and $7,300 for a family. 2. Consider a Roth. Transferring money in a traditional IRA to a Roth IRA is another tax saving tip. You'll pay taxes on the converted amount, but then the money has growth potential and can be withdrawn tax-free, and it isn't subject to a required minimum distribution for the life of the owner. Why consider a Roth IRA conversion now? First, with many investments down this year, you can convert more shares for the same total amount and same potential tax bill. Also, tax rates are set to increase in 2026, so you could end up paying higher rates later on conversions. 3. Defer some income. If you have freelance income, you could delay billing for your services until next year. Speak with your accountant to be sure if this is a good option for your situation. 4. Donate appreciated assets. Itemizers can also donate appreciated assets held longer than one year to a qualified public charity and deduct the fair market value of the asset without paying capital gains tax. The donation is subject to a 30% adjusted gross income (AGI) limitation. 5. Consider gifting to loved ones. You can gift up to $16,000 per recipient to as many people as you like. While you don't get an income tax deduction for such gifts, the recipient won't owe taxes, and the gift can help reduce the value of your estate, without using up your lifetime gift and estate tax exemption. Want to hear more year-end tax tips? Click on this link for more details and tips: Top Tax Tips for 2022 or contact our office at Brien@TraditionsWealthAdvisors.com or 979-694-9100 with questions.

0 Comments

Traditions Wealth Advisors

James Lane, Financial Analyst Intern Brien L. Smith, CFP®, CEO of TWA November 15, 2022 I. Summary: Introduction / Overview The November midterm elections have concluded (with the exception of the Georgia Senate runoff) and the Democrats are expected to retain the Senate while the Republicans have taken the House of Representatives. The vast majority of U.S. adults (82%) rated inflation as extremely important or very important for the government to address, according to a recent poll by Monmouth University. Comparatively, fewer respondents assigned such high ratings of importance to other hot-button issues such as abortion (56%), gun control (51%), and climate change (49%). How the midterm elections could impact the economy and your finances Democrats have held both chambers of Congress for the past two years — resulting in a government trifecta, which is when the executive branch and both legislative branch chambers are all controlled by the same political party. With the Republicans gaining the House of Representatives there is expected to be political gridlock, where there is difficulty passing legislation. Some feel a divided government would result in few meaningful steps to improve the economy. Bipartisan action after the midterms to combat inflation is expected to be difficult with a divided government, according to an August Wells Fargo Investment Institute report. A slight majority — 53 percent — of Americans felt the midterm election would result in divided government and gridlock, an October Axios/Ipsos poll found. One potential implication of the Republicans gaining control of the House of Representatives is that lawmakers may attempt to make the 2017 Republican tax cuts permanent in an effort to grow the economy and create jobs. Republicans may also seek to repeal the corporate tax hikes Biden signed into law in August. Republicans are also expected to push for increased U.S. oil production in an effort to achieve self-sufficiency for energy production. However, it will be difficult to pass such legislation given President Biden and the Democratic party’s position on oil and climate change. Democrats are expected to make further attempts to pass measures from Biden’s $1.7 trillion Build Back Better Act that did not make it into law. Critics of the Build Back Better Act — and its offshoot, the Inflation Reduction Act, which passed in August — argue that many of the measures are dedicated to spending money and are therefore bad for reducing inflation. The Build Back Better Act contained more than $1.7 trillion in economic and infrastructure proposals. It sought to lower education and healthcare costs, as well to extend the expanded child tax credit. It failed to make it through Senate, however, after facing opposition from some moderate Democratic Senators. The Inflation Reduction Act aims to lower inflation by reducing the deficit, curbing prescription drug costs, and investing in clean energy. It seeks to combat climate change by increasing reliance on renewable energy sources like wind and solar power, as well as reducing greenhouse gas emissions and fossil fuel pollution. The act would also increase the minimum tax rate to 15% for some large corporations. Taxes The November midterm elections will also help decide which tax priorities Democratic and Republican lawmakers pursue in the next couple of years. And those priorities could involve tax deductions and tax incentives that directly impact your finances. After the November midterm elections, Congress will need to come to an agreement on Fiscal Year 2023 spending. That creates an opportunity for a potential year-end tax package. There are several tax issues that Congress could address in such a package depending on their appetite for negotiation. For example, with Republicans now controlling the House of Representatives they may not be quick to support so-called lame-duck spending. That reluctance could be enhanced by the fact that the Democratic-controlled congress already passed the Inflation Reduction Act, which provides about $270 billion in clean energy tax incentives that include everything from electric vehicle tax credits to tax credits for energy efficient home improvements. Child Tax Credit The expanded child tax credit was enacted with the American Rescue Plan Act (ARPA) and allowed eligible families in 2021 to receive advanced payments of up to either $250 or $300 a month (per qualifying child), for six months, depending on the age of each child. Democrats and various advocacy organizations have pushed to reinstate the expanded credit, which some data show effectively helped to reduce the child poverty rate. Democrats are expected to push to reinstate the child tax credit. Inflation Reduction Act Implementation If Democrats are also expected to try and push the Inflation Reduction Act into law. Currently, the Treasury Department and the IRS are seeking public input to propose regulations to implement the many clean energy tax incentives in the new law. However, with Republicans taking control of the House, Minority Leader Kevin McCarthy (R-California) has vowed to block the $80 billion in funds allotted in the Inflation Reduction Act for the IRS. McCarthy and other Republican lawmakers have claimed that the funding will result in an “army” of 87,000 IRS agents coming to audit middle income Americans. Retirement Savings On the bright side, there appears to be bipartisan support for potentially major retirement legislation. The EARN act is designed to encourage small businesses to adopt retirement plans and make it easier for part-time workers to participate in retirement plans. The bill would also expand savers credit for low and middle-income workers and allow penalty free-withdrawals during certain emergencies. Congress will have to reconcile the EARN Act with bipartisan House-passed SECURE 2.0, which would also make significant changes to retirement plans including raising the age for taking required minimum distributions (RMDs). Trump Tax Cuts With Republicans gaining control of the U.S. House of Representatives, they have pledged to propose legislation to make the so-called Trump tax cuts permanent. The individual tax cuts were enacted with the Tax Cuts and Jobs Act of 2017 and many of the tax breaks tied to individuals are set to expire after 2025. In a pillar in the document that concerns the economy, Republicans say they will fight inflation and lower the cost of living in part through what they describe as a “pro-growth tax economy.” It’s unclear at this time what specific tax policies the GOP would pursue if they gained control of the House or the Senate. But President Biden would still have VETO power and Congressional override would be highly unlikely. State Tax Initiatives: Taxing The Rich There are tax initiatives on November midterm ballots in several states. For example, Bloomberg points out that California voters will be asked to consider Proposition 30 — whether wealthy Californians should pay more tax. Colorado voters will cast votes on whether proposed income tax cuts should limit tax deductions for wealthy residents. Notably, like many other states, California and Massachusetts are returning surplus revenue to their residents in 2022 through state “stimulus” checks. California’s second round of tax stimulus checks are underway, and Massachusetts is returning nearly $3 billion to eligible taxpayers with its 2022 Massachusetts tax refund, beginning in November and continuing through Mid-December. Overall, Congress has been divided and political gridlock is highly likely, and analysts are expecting no major legislation to get passed into law. Historically, the stock market has done better under a split government when a Democrat is in the white house. Average annual S&P 500 returns have been 14% in a split Congress under a democratic president, according to data since 1932 analyzed by RBC Capital Markets. That compares when democrats controlled the presidency and Congress. Financial anxiety is more severe than just worried about having enough money. It is a disorder that symptoms can include tension, irritability, and always worried. Financial anxiety can lead to people obsessing over checking their money or savings, imagining they don't have enough money, or avoid checking their finances all together. Click on the video below for strategies to help you cope with financial anxiety. The good news is that your social security payments will increase by a record amount next year. The bad news: your tax bill may also rise with it!

The cost of living adjustment (COLA) should increase retirees payments by 8.7% which will help alleviate some of the cost of inflation. Unfortunately, more retirees will owe taxes on Social Security benefits. Higher income means higher taxes but don't fret there are ways designed to plan for the tax increase and to help keep more of your retirement income next year. Here are some tips to discuss with your tax or financial advisor to prepare for these changes in 2023 and lower your income. First, minimize taxable traditional 401(k) or IRA withdrawals, as these are taxed as ordinary income, corresponding to your marginal tax bracket, but be sure to still withdraw enough to meet any required minimum distributions. Next, consider qualified withdrawals from a Roth IRA, a Roth 401(k), or a health savings account (HSA), which would not be subject to federal income tax and wouldn't have an impact on how your Social Security benefit is taxed. (Note: Roth IRA distributions of earnings must meet the 5-year aging requirement to be tax-free, and HSA withdrawals are only tax-free when used to pay for qualified health expenses.) Finally, withdrawals from a brokerage account, where long-term capital gains are taxed at a lower capital gains tax rate, generally between 0% and 20%, if you held the investments over a year. Figuring out withdrawals from retirement and brokerage accounts can be complicated, so it may help to work with an advisor. Further, while claiming your social security as soon as possible is tempting, it is still best to wait until your full retirement age of 67. Plus each year you delay until 70, increases your benefits 8%. 2023's cost of living adjustment can help you keep up with the higher costs. Make sure you are looking at your taxes long term and not just at this year. Whether you're planning for the next year or the next decade, managing taxes throughout retirement can be complicated. Be sure to work with a tax professional to help you understand the potential tax impacts of any planning decisions. Reach out to us for guidance and a referral at Brien@traditionswealthadvisors.com or 979-694-9100. These simple steps are what Traditions Wealth Advisors does daily to set your mind at peace with your investment results.

Step 1: Make a plan you CAN stick to. An investment plan takes many factors into consideration, such as your financial and retirement goals, your current savings, and your tolerance for unexpected market fluctuations. Once you determine your objectives, you can decide the best mix of investments to help you achieve them. Although it's natural to want the highest return possible from your portfolio, it's also important to consider the temporary losses you're willing to withstand in negative markets, so you're not tempted to abandon your investment plan during inevitable periods of anxiety and discomfort. Step 2: Rebalance periodically. After you determine your optimal mix of investments, you shouldn't need to make frequent changes to your portfolio. In fact, research has shown that trading too often can lead to underperformance over time. Still, as markets rise and fall, your asset allocation can drift from its original targets, changing the overall risk and return profile of your investment portfolio. To ensure your portfolio stays aligned with your future goals and risk tolerance--and to maximize your results over time--it's important to periodically take gains from investments that have risen in value and use the proceeds to buy more of the investments that have declined in value. Step 3: Check your account balances less. Nobel Prize-winning behavioral economists Richard Thaler and Amos Tversky found that investors who check their account balances frequently are less willing to take on risk, which ultimately causes them to fall short of their financial goals. A healthy amount of risk is necessary to grow your assets over the long term. If you're prone to panicking when markets fall, the best solution is to check your accounts no more than once per quarter. Further questions on these simple steps? Please contact us at Brien@TraditionsWealthAdvisors.com or 979-694-9100. I. Summary:

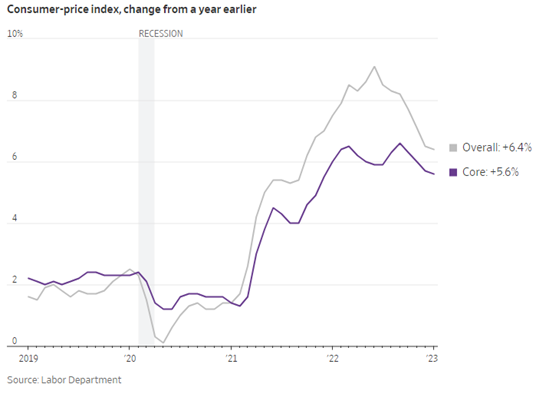

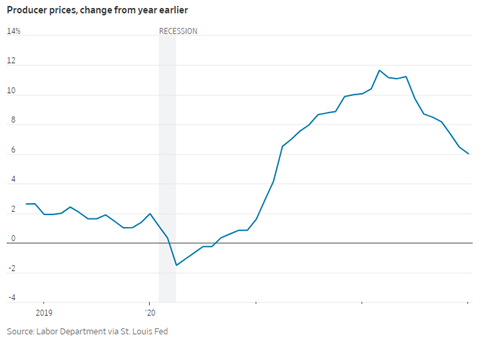

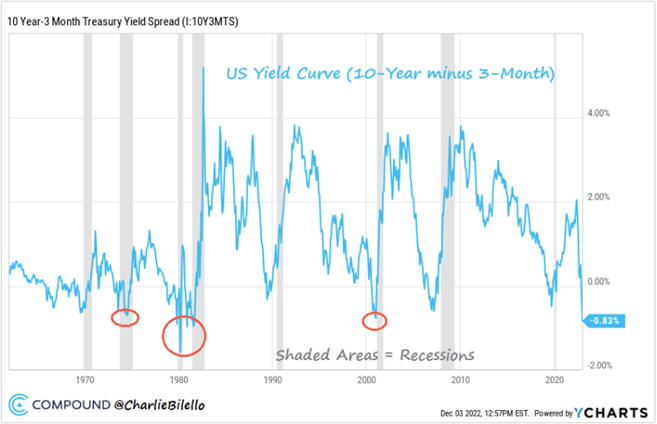

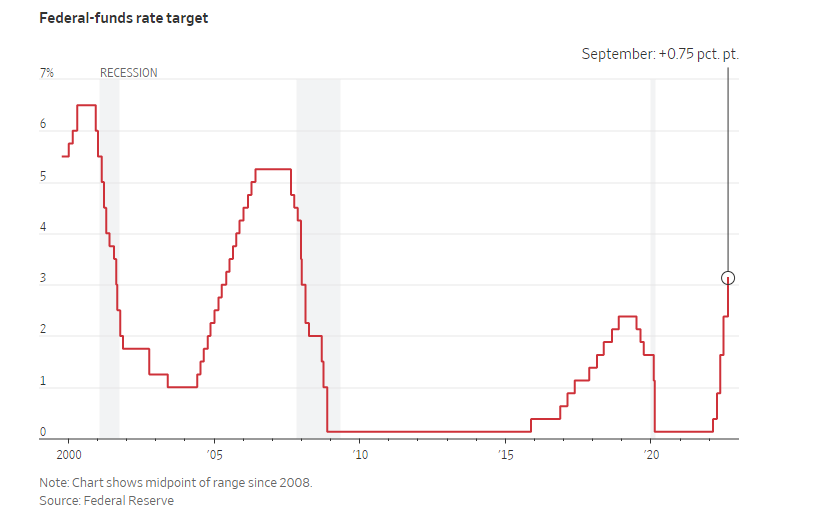

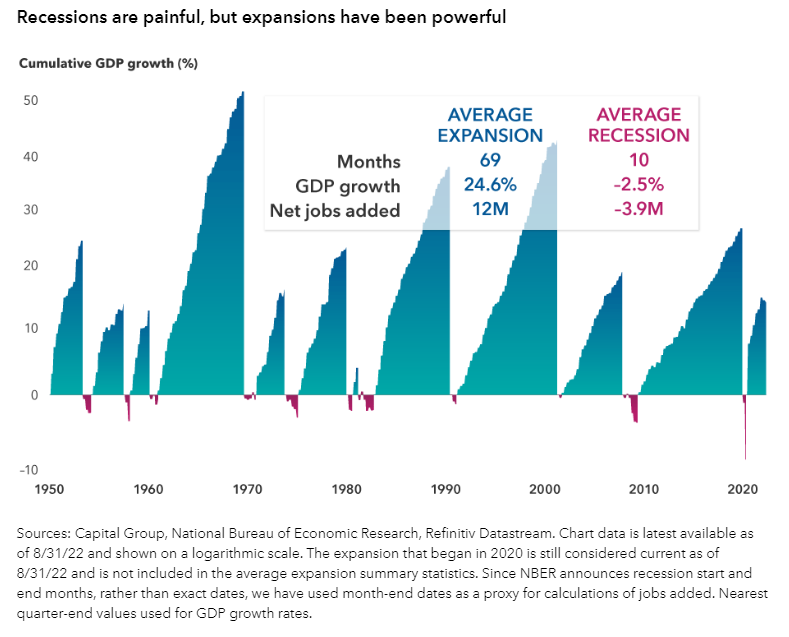

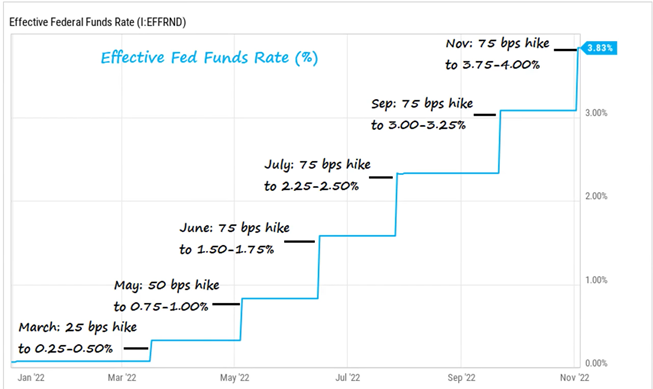

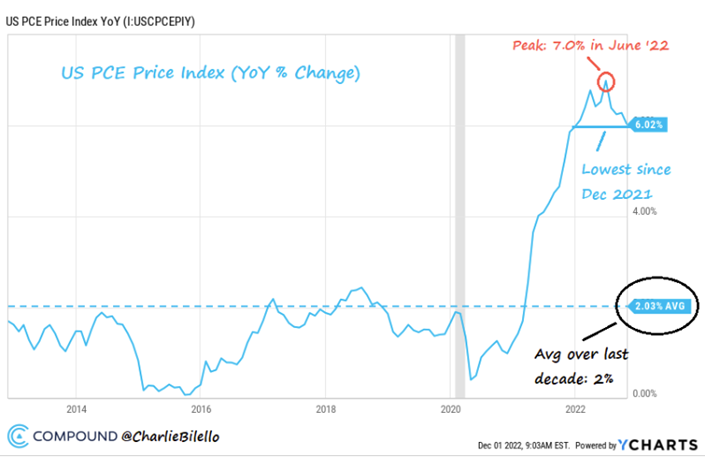

There is currently a lot of talk about a recession approaching by the end of this year and as a result, we have seen recent market selloffs as investors become worried about our economies future. The National Bureau of Economic Research (NBER) defines a recession as “a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production and wholesale-retail sales.” The source of these recessionary concerns stem from The Federal Reserve, which is currently increasing interest rates to slow down economic growth and combat high inflation levels. They are specifically increasing the federal funds rate. The federal funds rate refers to the interest rate that banks charge other institutions for lending out excess cash. The federal funds rate is important because the rate can determine how much it costs for you to borrow from the bank in the form of interest rates. The main goal of the Federal Reserve right now is to reduce rampant inflation by increasing interest rates and slowing down economic growth. Higher interest rates do not mean the economy suffer a major crash. An economic slowdown is necessary to ensure that price stability is maintained. Boston Federal Reserve President has recently said in a press conference that “history has shown that price stability is a precondition to achieving maximum employment over the medium and long term”. Therefore, short-term pain for consumers and businesses will be necessary to achieve the fed’s goal of 2% inflation. Many people within the Federal Reserve and outside experts believe that the damage to overall growth would be limited. In a recent press conference, the chairman of the Federal Reserve, Jerome Powell, stated that “Higher interest rates, slower growth, and a softening labor market are all painful for the public that we serve, but they’re not as painful as failing to restore price stability”. Making sure inflation can be controlled is painful for us as investors in the short term, but we believe it is necessary to foster a more stable future for long term investments.  Although many investors are becoming fearful of an imminent recession, economy and survey data have held up well. Healthy gains in employment and disposable personal income are fueling nominal consumer spending growth, and confidence in our economy has lifted. According to a credible source from Goldman Sachs, “The US economy has about a one in three chance of slipping into a mild recession by the middle of 2023”. A lot of economic experts are predicting a mild recession with only a limited increase in the unemployment rate of 1%. With economists and market experts predicting a shallow and mild recession, there is a good chance that this recession will not be nearly as painful as ones seen in the 1980s and 2007-2009.  More current evidence for a mild recession are unusually high level of job openings typically seen during a recession. This should dampen the recessionary effect of higher unemployment in the economy. Experts are also predicting that consumer spending will be higher than in past recessions. In other words, consumers may feel the effects of this recession much less than the recessions of the past. Another big reason to have optimism for the future is that there are many sectors in the economy that are currently growing and have room to normalize to their pre-pandemic levels, even during a recession. Due to the negative market effects we saw during the covid pandemic of 2020, sectors such as transportation services, tourism, and infrastructure were already negatively affected before the recent market selloff. Now that covid restrictions and have been lifted, these sectors have started recovering even among upcoming recession fears.

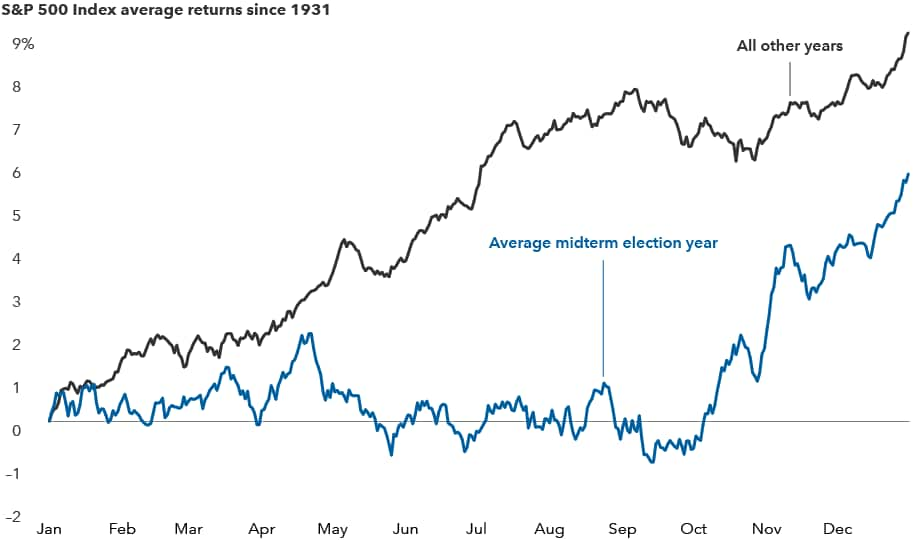

Randall Kroszner, former Federal Reserve governor, claims that “A U.S. recession this year or next is looking likely, but Americans can rest assured that the worst-case scenario of a ‘devastating early-1980s–type recession’ probably won’t come to pass”. The economic conditions of today are different from the past, therefore many experts are expecting the predicted recession to be very mild. A deep recession would only occur if inflation levels do not decline further by next year. The Federal Reserve would be forced to take even further action and increase interest rates more. Thankfully, this is highly unlikely as inflation has peaked and has been slowly declining after each inflation report. To combat the predicted mild recession, Traditions Wealth Advisors has been researching new potential investment opportunities for you, our valued clients. We have been avoiding and trimming our clients’ holdings in volatile growth funds and have placed an emphasis on value funds. Dividend stocks also provide a cushion for a portfolio during a recessionary period. Fixed income investment opportunities continue to remain as a solid income generator during slowdowns. We also have been researching investment opportunities in the real estate market, and have added TIAA-CREF Direct Real Estate to most of our clients’ portfolios, which has produced positive gains while most other asset classes have been hit hard. It is important as investors to not overreact to a recession and all the over-the-top news headlines. It is important to stay focused on long term investment goals and not make any decisions due to a short-term disruption. While control of Congress may be at stake, do midterm elections have any effect on markets? To find out, we examined more than 90 years of data and found that the answer is yes, markets have behaved differently during midterm election years. Here are five things you need to know about investing in this political cycle: 1. The president’s party typically loses seats in Congress Midterm elections occur at the midpoint of a presidential term and usually result in the president’s party losing ground in Congress. Over the past 22 midterm elections, the president’s party has lost an average 28 seats in the House of Representatives and four in the Senate. Only twice has the president’s party gained seats in both chambers. Why is this usually the case? First, supporters of the party not in power usually are more motivated to boost voter turnout. Also, the president’s approval rating typically dips during the first two years in office, which can influence swing voters. Since losing seats is so common, it’s usually priced into the markets early in the year. However, the extent of a political power shift — and the resulting policy impacts — remain unclear until later in the year, which can explain other trends we’ve uncovered. 2. Market returns tend to be muted until later in midterm years  Our analysis of returns for the S&P 500 Index since 1931 revealed that the path of stocks throughout midterm election years differs noticeably compared to all other years. Since markets typically rise over long periods of time, the average stock movement during an average year should steadily increase. We found that in the first several months of years with a midterm election, stocks have tended to have lower average returns and often gained little ground until shortly before the election. Markets don’t like uncertainty — and that adage seems to apply here. Earlier in the year there is less certainty about the election’s outcome and impact. But markets have tended to rally in the weeks before an election, and they have continued to rise after the polls close. So far, 2022 has been another example of a midterm election year with lackluster returns, although the impact of politics has been minimal compared to that of inflation and rising rates. Despite the uncertainty, investors shouldn’t sit on the sidelines or try to time the market. The path of stocks varies greatly each election cycle, and the overall long-term trend of markets has been positive. 3. Midterm election years have had higher volatility Elections can be tough on the nerves. Candidates often draw attention to the country’s problems, and campaigns regularly amplify negative messages. Policy proposals may be unclear and often target specific industries or companies. It may come as no surprise then that market volatility is higher in midterm election years, especially in the weeks leading up to Election Day. Since 1970, midterm years have a median standard deviation of returns of nearly 16%, compared with 13% in all other years. 4. Market returns after midterm elections have been strong  The silver lining for investors is that markets have tended to rebound strongly in subsequent months, and the rally that has often started shortly before Election Day hasn’t been just a short-term blip. Above-average returns have been typical for the full year following the election cycle. Since 1950, the average one-year return following a midterm election was 15%. That’s more than twice the return of all other years during a similar period. Of course every cycle is different, and elections are just one of many factors influencing market returns. For example, over the next year investors will need to weigh the impacts of a potential U.S. recession and global economic and geopolitical concerns 5. Stocks have done well regardless of the makeup of Washington  There’s nothing wrong with wanting your preferred candidate to win, but investors can run into trouble if they place too much importance on election results. That’s because, historically, elections have had little impact on long-term investment returns. In 2020, many investors feared the “blue wave” scenario, or Democratic sweep. But despite these concerns, the S&P 500 rose 42% in the 14 months following the 2020 election (from November 4, 2020, through January 3, 2022). Going back to 1933, markets have averaged double-digit returns in all years that a single party controlled the White House and both chambers of Congress. This is just below the average gains in years with a split Congress, a scenario which many believe is a strong possibility this year. Even the “least good” outcome — when the president’s opposing party controls Congress — notched a solid 7.4% average price return.

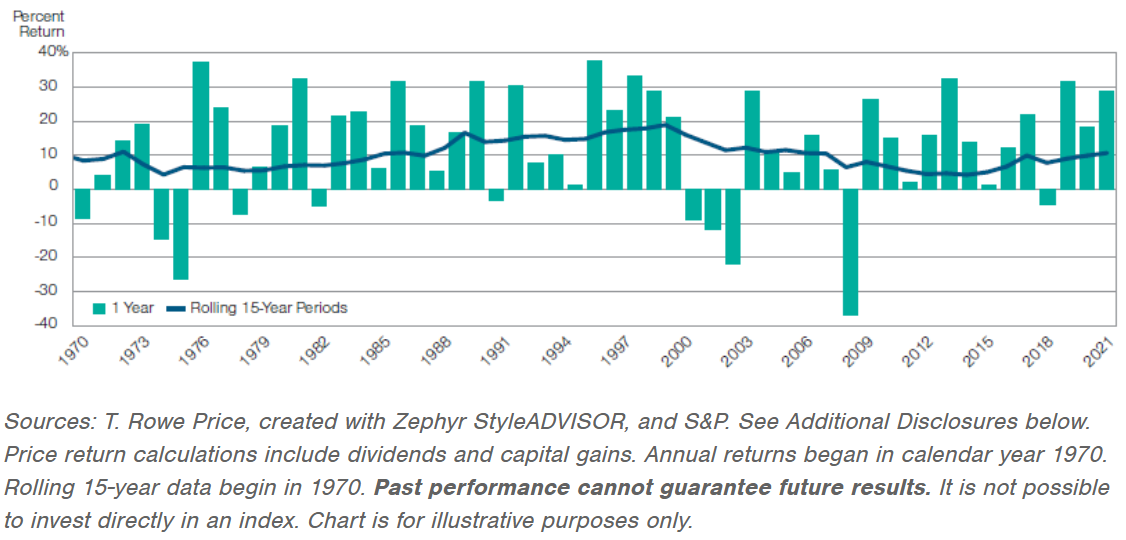

What’s the bottom line for investors? Midterm elections — and politics as a whole — generate a lot of noise and uncertainty. Even if elections spur higher volatility there is no need to fear them. The reality is that long-term equity returns come from the value of individual companies over time. Smart investors would be wise to look past the short-term highs and lows and maintain a long-term focus. For further questions about the markets and this article, please reach out to Traditions Wealth Advisors at 979-694-9100 or Brien@TraditionsWealthAdvisors.com Source: Buchbinder, Chris. Miller, Matt. 8 September 2022. Can midterm elections move markets? 5 charts to watch. https://www.capitalgroup.com/ria/insights/articles/midterm-elections-markets-5-charts-sept-2022.html?sfid=504078533&cid=80828184&et_cid=80828184&cgsrc=SFMC&alias=B-btn-LP-MidtermElectionsMarkets It may be tempting to take money out of the stock market. Sticking to a long-term plan is usually best. It can be hard to stay the course. Acting on emotion or trying to anticipate the market’s direction can compromise a portfolio’s long-term return potential. In general, having an asset allocation aligned with the time horizon of an investor’s goals is the most prudent path. Staying the course takes patience and discipline and can be especially difficult during times of uncertainty. Investors with a healthy dose of equities in their portfolio are likely to benefit from the long-term growth potential of stocks since, over time, the magnitude of market gains has been significantly greater than that of losses. Of course, past performance cannot guarantee future results. Remaining invested through downturns and corrections may allow investors to take advantage of long-term growth potential.  While it may be challenging to stick with a long-term strategy, doing so means an investor could be well positioned to reap potential gains as the market recovers.

In times of market volatility, it’s impossible to know when it may end. Investors who feel a strategy change is in order could consider gradual adjustments. They could also wait until the volatility subsides to make wholesale shifts to their strategy. “These are challenging times for many people,” says Judith Ward, CFP® of T. Rowe Price. “If investors control the important things, such as how much to save and spend, and position their investments to balance this short-term volatility with longer-term growth, they can give themselves the best chance to achieve a comfortable retirement.” Questions about your portfolio and staying the course article? Contact Brien@TraditionsWealthAdvisors.com Source: T. Rowe Price. 25 July 2022. Personal Finance. https://www.troweprice.com/personal-investing/resources/insights/does-staying-the-course-still-make-sense.html?cid=PI_Single_Topic_NonSubscriber_ACC_PRE_EM_202207&bid=1046947328&PlacementGUID=em_PI_PI_Single_Topic_EM_NonSubscriber_202207-PI_Single_Topic_NonSubscriber_ACC_PRE_EM_202207_20220728&b2c-uber=u.4BDAB1C8-0F6B-9872-F733-7678B43EBF89 |

Let our team work for you. Call 979-694-9100 or

email Michael@TraditionsWealthAdvisors.com

|

TRADITIONS WEALTH ADVISORS

2700 Earl Rudder Frwy South, Ste. 2600 College Station, TX 77845 |

VISIT OUR BLOG: Stay current with industry news and tips.

|